Business Plan for Partnership Firm

A business plan for partnership firm is recommended for anyone entering into a business partnership. 3 min read updated on November 02, 2020

A business plan for a partnership firm is recommended for anyone entering into a business partnership. A business partnership is two or more people working together to run a business. Each person takes on equal risks and rewards that come from the business. A proper business plan is ideal for handling current and future business decisions.

Steps For Planning a Business Partnership

- Write a mission statement to clearly state the direction and goals the business plans to take. By writing a mission statement, the partners agree to the company's direction now and in the future.

- Develop a reimbursement plan for the costs and investments incurred during startup. The amount of money provided for the startup is not always equal. Therefore, it is beneficial to make a plan that takes this into account with repayment and returns on investment. Avoiding arguments over the value of the startup amount versus levels of sweat equity will be removed with a reimbursement plan.

- Create a method to resolve partner disputes. If an odd number of members are part of the partnership, you can choose to vote democratically. In the case of two partners, the partners may split areas of the business having the final say. For example, one person can make final decisions on marketing and sales planning, while the other person makes final decisions on financial planning.

- Appoint an outside panel of advisors, or ombudsman , to resolve any internal disputes. Trusted experts should always be used to avoid ruining the partner relationship.

- Divide all the responsibilities of the partners related to labor and management and assign the amount of compensation they will receive. The compensation is not always equal based on the workload the partner takes on.

- Request that outside experts review the partnership agreement for any legal or accounting mistakes. The experts may be able to point out unknown problems that exist in the agreement. This review should take place before the partnership begins business operations.

Partnership Deed

A partnership deed and partnership agreement are the same, but the partnership deed is in writing . A partnership agreement can exist solely through verbal communications or actions. A partnership deed is recommended for businesses as it clearly defines the terms of the partnership.

The partnership deed helps prove the agreed-upon terms if there are any conflicts. Without a deed, the rules to settle disputes will fall to the state laws where the partnership exists. This creates another issue where one partner may file suit to benefit from the existing laws. Legal action can be avoided with a partnership deed that lists all details of the business that the partners agreed to when they began the business.

Partner Business Plans

When legal firms are looking to add a new partner, a well-written business plan that shows the new partners' intent to grow the business will make them stand out from the rest of the applicants. The business plan should exceed the expectations of the firm.

The key elements of the business plan are:

- Create an introduction that details your professional history, areas of expertise, and why you are the right fit for the firm.

- Provide market research and analysis of the needs of the local area, what competition exists, and why the firm offers the best way to reach this marketplace.

- Describe your current client base, prospective clients, and untapped areas you'd like to reach.

- Include any cross-selling opportunities that exist with current and prospective clients.

- Share ways you can develop business sources including publications, speeches, client seminars, newsletters, and similar.

- Explain your long-term strategy to meet the goals and targets that will benefit the firm.

- Show a history of collections, billing rates, and billable hours and projections for the current year, three-years, and five-years.

- Time the partners must invest.

- Key staff will be needed (paralegals, secretaries, etc.)

- Travel expenses.

- Marketing materials,

- Presentations.

- Foreign language skill requirements.

End with a conclusion that is creative recaps the important points in the plan, what value will be added to the firm, and why you are the best fit for the firm.

If you need help with a business plan for a partnership firm, you can post your legal need on UpCounsel's marketplace. UpCounsel accepts only the top 5 percent of lawyers to its site. Lawyers on UpCounsel come from law schools such as Harvard Law and Yale Law and average 14 years of legal experience, including work with or on behalf of companies like Google, Menlo Ventures, and Airbnb.

Hire the top business lawyers and save up to 60% on legal fees

Content Approved by UpCounsel

- Limited Partnership Rules: Everything You Need To Know

- Purpose of Partnership: Everything You Need To Know

- Authority of Partners in Partnership: What You Need to Know

- Partnership Agreement Between Company and Individual

- Limited Company Partnership Agreement

- How to Make a Partnership Agreement Legally Binding?

- Contract for Business Partners

- Disadvantages of Partnership

- General Partnership

- Partnership and Company

How to Write a Business Partnership Proposal {Template Included}

A business partnership proposal serves as the first impression of your business philosophy, your understanding of the partnership’s potential, and your vision for mutual growth. It’s not just about presenting what your business can offer, but also about showing that you understand and respect the needs and goals of your potential partner. A well-written proposal can be the key to unlocking fruitful collaborations, opening doors to shared resources, expertise, and markets, thus paving the way for substantial business growth and success.

This article is designed as a comprehensive guide to help you create an impactful business partnership proposal. Ready to write a business partnership proposal? Let’s get started.

Understanding Your Audience

Identifying Potential Partners

The first step in writing a business partnership proposal is to identify the right potential partners. This process involves more than just finding businesses that align with your industry or market. It’s about seeking out companies or individuals who share similar values, goals, and visions. Look for partners who complement your business’s strengths and can help mitigate its weaknesses. This might mean a partner with a strong presence in a market you’re trying to enter or one with access to resources that can help scale your business. Identifying the right partner is crucial as it sets the tone for the entire proposal and the potential partnership.

When identifying potential partners, consider:

– Industry Relevance: Partners in the same or complementary industries are more likely to understand and value your proposal.

– Market Position: Consider how a partner’s market position could benefit your business. For instance, a partnership with a well-established player can offer credibility, while teaming up with an innovative newcomer can provide fresh perspectives.

– Cultural Fit: Aligning with a partner who shares similar business ethics and corporate culture can lead to a smoother collaboration.

– Long-Term Potential: Look for partners who are not just beneficial for a one-time project but could lead to long-term collaboration.

Researching Their Needs and Interests

After identifying potential partners, the next step is to research their specific needs and interests. This research is important as it helps tailor your proposal to address the specific challenges or opportunities your potential partner is facing. By demonstrating that you understand and can provide solutions to their needs, your proposal will be more persuasive and relevant.

To effectively research their needs and interests:

– Review Their Business Model: Understand how they operate, their revenue streams, and their customer base. This helps in aligning your proposal with their business strategy.

– Analyze Their Market Position: Look at their market share, competitors, and industry trends. This insight can help you position your partnership as a solution to specific market challenges they might be facing.

– Understand Their Goals: Whether it’s expansion, diversification, or sustainability, knowing what your potential partner aims to achieve can help you tailor your proposal to align with these goals.

– Use Social Media and Publications: Review their social media platforms, press releases, and industry publications for recent announcements, challenges they’re addressing, or initiatives they’re undertaking. This can provide clues to their current focus and future plans.

– Networking and Direct Communication: Sometimes, the best information comes from direct interaction. Attend industry events, engage in networking opportunities, or even reach out directly to understand their vision and objectives better.

Key Components of a Business Partnership Proposal

Executive Summary

The executive summary is the cornerstone of your business partnership proposal. It should provide a concise, compelling overview of what the proposal entails and why it’s beneficial for both parties. This section is often the first (and sometimes the only) part read by decision-makers, so it needs to be clear, engaging, and persuasive. Highlight the key aspects of the partnership, including the goals, the value proposition, and the main benefits for both parties. The executive summary should be a standalone document that encapsulates the essence of the proposal, compelling the reader to delve deeper into the details.

Business Objectives

This section should outline the specific objectives you hope to achieve through the partnership. Clear, measurable, and realistic goals show a potential partner that you have a well-thought-out plan for the partnership’s success. These objectives could range from expanding into new markets, leveraging each other’s customer base, to combining resources for a new venture. Be specific about what success looks like and how it will be measured. This clarity will help align both parties’ expectations and form the basis for a productive relationship.

Value Proposition

Your value proposition is arguably the most crucial part of the proposal. This is where you articulate the unique benefits that your company brings to the table and why this partnership is advantageous for your potential partner. It should clearly demonstrate how the partnership will create added value for both parties, whether through increased revenue, market expansion, enhanced capabilities, or other strategic advantages. A strong value proposition is tailored to your potential partner’s needs and goals, showing that you have done your homework and understand what they are looking for in a partnership.

Partnership Details

In this section, delve into the specifics of how the partnership will work. Outline the roles and responsibilities of each party, the governance structure of the partnership, and how decisions will be made. Include details about resource allocation, timelines, and project management. If there are any specific projects or initiatives that will kick off the partnership, describe them in detail here. Providing a clear and detailed plan shows that you are serious about the partnership and have considered how to make it successful.

Financial Projections

Financial projections are essential in any business proposal . This section should provide an analysis of the expected financial outcomes of the partnership. Include revenue forecasts, cost analysis, and any investments required from both parties. If possible, use data and analytics to back up your projections. Be realistic and conservative in your estimates. Providing a clear financial picture helps both parties understand the economic implications of the partnership and aids in decision-making.

Legal and Ethical Considerations

In this part of the proposal, address any legal and ethical considerations relevant to the partnership. This might include compliance with industry regulations, intellectual property rights, confidentiality agreements, and any other legal obligations. It’s also important to discuss how ethical considerations will be handled, reflecting a commitment to corporate social responsibility. Addressing these issues upfront builds trust and shows that you are committed to maintaining a professional and ethical business relationship.

Each of these components plays a crucial role in developing a comprehensive and convincing business partnership proposal. They collectively demonstrate your understanding of what it takes to build a successful partnership, reflecting both strategic foresight and attention to detail.

Writing the Business Partnership Proposal

Starting with a Strong Introduction

The introduction of your proposal is where you make your first impression. It sets the tone for the rest of the document and should immediately capture the interest of the reader. A strong introduction goes beyond a simple greeting or a statement of purpose; it should hook the reader by presenting the idea of the partnership, its relevance, and why it matters. This section should echo the excitement and potential you see in the partnership, making it clear why the reader should be interested in what you have to say. Consider starting with a compelling fact, a brief story, or a poignant question that relates directly to the potential partner’s needs or challenges, thus creating a direct connection from the outset.

Clear and Concise Language

The effectiveness of your proposal largely depends on how easily it can be read and understood. Use clear, concise language to ensure your message is conveyed effectively. Avoid jargon and technical terms that might not be familiar to all readers, unless they are industry-standard and necessary. Your aim should be to make the proposal as accessible as possible, so it speaks to decision-makers at all levels. Short, to-the-point sentences are often more powerful than lengthy, complex ones. Remember, clarity and brevity do not mean oversimplifying your ideas; rather, it’s about presenting them in a manner that is easy to grasp and remember.

Personalizing the Proposal

Personalization can significantly increase the impact of your proposal. This involves tailoring the content to directly address the specific needs, interests, and circumstances of the potential partner. Refer to their recent achievements, current projects, or particular challenges they are facing. This shows that you have taken the time to understand them and have thought deeply about how the partnership can be beneficial. Personalization can be achieved through the language you use, the examples you cite, and the specific benefits you highlight. By making the proposal as relevant as possible to the potential partner, you increase the likelihood of engaging their interest and winning their buy-in.

Check out this partnership proposal template from Prospero: https://goprospero.com/proposal/partnership-proposal-template/

Business Partnership Proposal Design and Presentation

Importance of a Professional Look

The design and overall presentation of your business partnership proposal can significantly influence its reception. A professional look not only reflects the seriousness and professionalism of your intent but also helps in making the document more readable and engaging. Attention to detail in the layout, font choice, color scheme, and formatting can make a substantial difference. It’s crucial that the proposal looks organized and aesthetically pleasing.

A well-designed proposal indicates that you have invested time and effort into its preparation, which can leave a lasting impression on the potential partner. This professionalism in presentation extends to ensuring that the document is free of errors, with consistent formatting throughout, further reflecting the quality and reliability of your business.

Using Visuals and Branding

Incorporating visuals and branding elements into your proposal can greatly enhance its impact. Visuals, such as charts, graphs, and images, can help to break up text, making the proposal more engaging and easier to digest. They can also be used effectively to illustrate points, showcase data, or convey complex information in a more accessible way. Branding elements, like your company’s logo and color scheme, help in reinforcing your identity and create a sense of familiarity, especially if the potential partner is already aware of your brand.

However, it’s important to use visuals judiciously. Every image or graph included should serve a clear purpose, such as emphasizing a point or explaining a concept more clearly. The key is to strike a balance – the proposal should be visually appealing and branded, but not so heavily designed that it distracts from the core message.

Business Partnership Proposal Follow-Up Strategies

Post-Submission Follow-Up

Once your proposal has been submitted, the follow-up process plays a crucial role in showing your continued interest and commitment. It’s important to plan and execute a follow-up strategy that is persistent yet respectful. Initially, a simple thank-you message acknowledging their time and consideration in reviewing your proposal can set a positive tone. Afterwards, it’s advisable to wait a reasonable period before following up again, typically a week or two, depending on the nature of the proposal and the urgency of the partnership.

During follow-up communications, it’s important to:

– Reiterate Key Points: Briefly remind them of the most compelling aspects of your proposal.

– Be Open to Discussion: Indicate your willingness to discuss any aspects of the proposal in more details if needed.

-Show Flexibility: Express your readiness to modify aspects of the proposal to better align with their needs or concerns.

Follow-up can be conducted through various channels such as email, phone calls, or even in-person meetings, depending on the level of relationship you have with the potential partner and the formality of the situation.

In conclusion, a business partnership proposal is a strategic document that requires careful thought, detailed planning, and a tailored approach. By following these guidelines, you can create a proposal that lays the foundation for a mutually beneficial business relationship.

Even though this might seem like a lot to handle, remember you don’t have to do it all by yourself. A good place to start is to use a template and a proposal tool like Prospero can really help. Prospero offers different templates and helpful features that can make writing your next proposal a lot easier and better!

Sign up for Prospero today

ABOUT THE AUTHOR

Damilola Oyetunji

Related posts.

7 Tips On Writing Better Website Design Proposals

How to Write a Cleaning Services Business Proposal

4 Best GetAccept Alternatives to Try Now

Top 10 PandaDoc Alternatives to Consider in 2024

| You might be using an unsupported or outdated browser. To get the best possible experience please use the latest version of Chrome, Firefox, Safari, or Microsoft Edge to view this website. |

How To Write A Business Plan (2024 Guide)

Updated: Apr 17, 2024, 11:59am

Table of Contents

Brainstorm an executive summary, create a company description, brainstorm your business goals, describe your services or products, conduct market research, create financial plans, bottom line, frequently asked questions.

Every business starts with a vision, which is distilled and communicated through a business plan. In addition to your high-level hopes and dreams, a strong business plan outlines short-term and long-term goals, budget and whatever else you might need to get started. In this guide, we’ll walk you through how to write a business plan that you can stick to and help guide your operations as you get started.

Featured Partners

ZenBusiness

$0 + State Fees

Varies By State & Package

On ZenBusiness' Website

On LegalZoom's Website

Northwest Registered Agent

$39 + State Fees

On Northwest Registered Agent's Website

$0 + State Fee

On Formations' Website

Drafting the Summary

An executive summary is an extremely important first step in your business. You have to be able to put the basic facts of your business in an elevator pitch-style sentence to grab investors’ attention and keep their interest. This should communicate your business’s name, what the products or services you’re selling are and what marketplace you’re entering.

Ask for Help

When drafting the executive summary, you should have a few different options. Enlist a few thought partners to review your executive summary possibilities to determine which one is best.

After you have the executive summary in place, you can work on the company description, which contains more specific information. In the description, you’ll need to include your business’s registered name , your business address and any key employees involved in the business.

The business description should also include the structure of your business, such as sole proprietorship , limited liability company (LLC) , partnership or corporation. This is the time to specify how much of an ownership stake everyone has in the company. Finally, include a section that outlines the history of the company and how it has evolved over time.

Wherever you are on the business journey, you return to your goals and assess where you are in meeting your in-progress targets and setting new goals to work toward.

Numbers-based Goals

Goals can cover a variety of sections of your business. Financial and profit goals are a given for when you’re establishing your business, but there are other goals to take into account as well with regard to brand awareness and growth. For example, you might want to hit a certain number of followers across social channels or raise your engagement rates.

Another goal could be to attract new investors or find grants if you’re a nonprofit business. If you’re looking to grow, you’ll want to set revenue targets to make that happen as well.

Intangible Goals

Goals unrelated to traceable numbers are important as well. These can include seeing your business’s advertisement reach the general public or receiving a terrific client review. These goals are important for the direction you take your business and the direction you want it to go in the future.

The business plan should have a section that explains the services or products that you’re offering. This is the part where you can also describe how they fit in the current market or are providing something necessary or entirely new. If you have any patents or trademarks, this is where you can include those too.

If you have any visual aids, they should be included here as well. This would also be a good place to include pricing strategy and explain your materials.

This is the part of the business plan where you can explain your expertise and different approach in greater depth. Show how what you’re offering is vital to the market and fills an important gap.

You can also situate your business in your industry and compare it to other ones and how you have a competitive advantage in the marketplace.

Other than financial goals, you want to have a budget and set your planned weekly, monthly and annual spending. There are several different costs to consider, such as operational costs.

Business Operations Costs

Rent for your business is the first big cost to factor into your budget. If your business is remote, the cost that replaces rent will be the software that maintains your virtual operations.

Marketing and sales costs should be next on your list. Devoting money to making sure people know about your business is as important as making sure it functions.

Other Costs

Although you can’t anticipate disasters, there are likely to be unanticipated costs that come up at some point in your business’s existence. It’s important to factor these possible costs into your financial plans so you’re not caught totally unaware.

Business plans are important for businesses of all sizes so that you can define where your business is and where you want it to go. Growing your business requires a vision, and giving yourself a roadmap in the form of a business plan will set you up for success.

How do I write a simple business plan?

When you’re working on a business plan, make sure you have as much information as possible so that you can simplify it to the most relevant information. A simple business plan still needs all of the parts included in this article, but you can be very clear and direct.

What are some common mistakes in a business plan?

The most common mistakes in a business plan are common writing issues like grammar errors or misspellings. It’s important to be clear in your sentence structure and proofread your business plan before sending it to any investors or partners.

What basic items should be included in a business plan?

When writing out a business plan, you want to make sure that you cover everything related to your concept for the business, an analysis of the industry―including potential customers and an overview of the market for your goods or services―how you plan to execute your vision for the business, how you plan to grow the business if it becomes successful and all financial data around the business, including current cash on hand, potential investors and budget plans for the next few years.

- Best VPN Services

- Best Project Management Software

- Best Web Hosting Services

- Best Antivirus Software

- Best LLC Services

- Best POS Systems

- Best Business VOIP Services

- Best Credit Card Processing Companies

- Best CRM Software for Small Business

- Best Fleet Management Software

- Best Business Credit Cards

- Best Business Loans

- Best Business Software

- Best Business Apps

- Best Free Software For Business

- How to Start a Business

- How To Make A Small Business Website

- How To Trademark A Name

- What Is An LLC?

- How To Set Up An LLC In 7 Steps

- What is Project Management?

- How To Write An Effective Business Proposal

How To Start A Business In Oklahoma (2024 Guide)

How To Get A Business License in Rhode Island (2024)

Best Montana Registered Agent Services Of 2024

Best Iowa Registered Agent Services Of 2024

Best Idaho Registered Agent Services Of 2024

Best Kentucky Registered Agent Services Of 2024

Julia is a writer in New York and started covering tech and business during the pandemic. She also covers books and the publishing industry.

How to Write a Partnership Proposal [Examples + Template]

Published: June 18, 2024

Partnerships generate $3.9 billion per year in the U.S. and supercharge the revenue of companies like Microsoft, Atlassian, and Shopify. Teaming up with another professional or company can multiply your capacity, expertise, and growth.

With so much at stake, approaching a potential partner can be intimidating. Whenever I make a business pitch, there are three items I work to perfect. First, an underlying relationship to build on. Second, a stellar verbal presentation for a pitch meeting. And third, a killer partnership proposal.

A partnership proposal is a powerful tool to showcase your professionalism and convince your potential partner why they should collaborate with you. I’ve compiled what you should include in your proposal, plus four partnership proposal templates to give you a head start.

What is a partnership proposal?

- Types of Partnership Proposals

Components of a Partnership Proposal

How to write a partnership proposal, partnership proposal template, partnership proposal examples, partnership proposal tips.

A partnership proposal is a document outlining the benefits, scope, and structure of a future collaboration between two businesses or individuals.

Most partnership collaborations begin with an idea and verbal discussions. “ Hey, here’s a crazy idea. What if we…” If you don’t know the person, start with a warm intro email or phone call first.

A partnership proposal is the next step in the process, formalizing concepts to align goals and gain buy-in. While it isn’t a legal contract, it’s often a precursor to one.

Free Business Proposal Template

Propose your business as the ideal solution using our Free Business Proposal Templates

- Problem summary

- Proposed solution

- Pricing information

- Project timeline

Download Free

All fields are required.

You're all set!

Click this link to access this resource at any time.

Types of Business Partnerships

Before creating a business partnership proposal, it’s important to understand which type of partnership you want to pursue.

General Business Partnership

When two or more individuals enter a business agreement and share unlimited liability, you have a general business partnership. A proposal for a general business partnership should include the share of ownership, contributions of each partner, the distribution of profits and losses, and the terms for dissolution.

Joint Venture

A joint venture (JV) is an agreement between two companies to combine resources and expertise for a specific purpose. For instance, a global company might form a JV with a local company when bringing a product to a new country.

Limited Partnership

A limited partnership (LP) is a business partnership that includes at least one general partner and at least one limited partner. Limited partners have minimal liability and management oversight of the operations. An LP is common in single-purpose scenarios like a real estate transaction.

Limited Liability Partnership

The LLP structure is common in professional service fields such as law firms, doctor’s offices, and accounting. Similar to an LLC, a limited liability partnership (LLP) is an agreement between partners that grants them limited liability. LLP requirements vary by state.

Influencer Partnership

An influencer partnership is a limited-scope agreement between an influencer or creator and a brand to create and publish branded social media content.

Sponsorship Partnership

A sponsorship is a collaboration between businesses, nonprofits, or media companies where one company pays for access to promote their goods and services to the other company’s audience.

When I write proposals, I always aim to personalize each one and find the right balance between personable and professional. While the nuances of each partnership model vary, there are a few common elements that every partnership business proposal should have.

Executive Summary

Hook your reader’s attention with a summary explaining the partnership concept, key benefits, and a table of contents.

List each partner with their contact and background information. Specify the role each will have, and whether they are a general or limited partner. Make it visual, with photos or logos.

Goals and Objectives

All good partnerships start with shared goals. Explain your goals and dreams for the partnership, from a high-level vision to specific objectives.

Share who your audience is and any key demographics. Make sure that your audience will fit with the partner’s audience, and vice-versa. An audience is a key selling point for partners, especially with influencer or sponsorship partnerships. Some brands go as far as account mapping to identify customer overlap, but general audience data can be as effective.

Scope of Work

Next, define the scope of work and projects to be covered with the partnership. If this is for a limited-scope project like an influencer collaboration, give a precise breakdown of project steps. If this is for a general partnership, JV, or LP, list target activities and deliverables and who is responsible for each. Give timelines as appropriate.

Benefits and Challenges

If you’ve ever written a business plan, you’re likely already familiar with the SWOT analysis (strengths, weaknesses, opportunities, threats). Similar to this, give an abbreviated analysis of:

- Challenges that will need to be tackled.

- Benefits to the collaboration.

- Market research and industry analysis.

Legal and Financial Information

Propose terms and conditions for the partnership, like payment and revenue-sharing structures. Spell out who will own intellectual property generated by the company and how royalties will be distributed. Address how disputes or a partnership dissolution would be handled.

To test this out, I wrote a general partnership proposal between a web designer and a web developer who want to team up to start a website studio. I used HubSpot’s partnership business proposal template to build a professional proposal outlining the partnership benefits and structure.

Creating a compelling partnership proposal requires a clear understanding of your potential partner's needs and how your collaboration can meet those needs. To simplify this process and ensure you have all the required information, consider using HubSpot Sales Software . This tool can help you gather insights, track interactions, and manage your proposal process more efficiently.

Here are the steps I took to create the proposal.

1. Outline the Benefits

To convince your partner, make the case why it’s worth them sharing their time (and profits) with you.

I started my proposal with an executive summary envisioning why the partnership would appeal to future clients. That leads into a “Benefits of Collaboration” section where I clearly outline the mutual advantages.

Don't forget to share this post!

Related articles.

10 Best Payroll Services for Startups

![How to Write an Investment Proposal [Template + Examples]](https://www.hubspot.com/hubfs/ft-investment.webp "how to write a business plan for a partnership")

How to Write an Investment Proposal [Template + Examples]

16 Examples of Positioning Statements & How to Craft Your Own

Startup Due Diligence: What it Is & Why it Matters

What is a Go-to-Market Strategy? GTM Plan Template + Examples

![300+ Business Name Ideas to Inspire You [+7 Brand Name Generators]](https://www.hubspot.com/hubfs/business-name-ideas_17.webp "how to write a business plan for a partnership")

300+ Business Name Ideas to Inspire You [+7 Brand Name Generators]

The Importance of Having a Startup Exit Strategy

10 Top Tech Startups To Watch

The Biggest Pros and Cons of Working for a Startup

15 Startup Newsletters for Entrepreneurs

Propose your business as the ideal solution using this free template.

Powerful and easy-to-use sales software that drives productivity, enables customer connection, and supports growing sales orgs

- IT/Operations

- Professional Services & Consulting

- IT and Software Solutions

- Facilities & Maintenance

- Infrastructure & Construction

Want help from the experts?

We offer bespoke training and custom template design to get you up and running faster.

- Books & Guides

- Knowledge Base

State of Proposals 2024

Distilling the data to reveal our top tips for doing more business by upping your proposal game.

- Book a Demo

How to Create a Partnership Proposal [With Free Template]

When embarking on a business partnership, expect challenges. Partners have different personalities, working styles, daily schedules, and initial investments. You need to juggle working together (possibly for the first time) while addressing market needs and differentiating yourself from competitors.

A partnership proposal can help make those challenges a little less daunting by clarifying the details of your collaboration before you even launch your business. It can get everyone on the same page, reducing the risks of detrimental disagreements later on.

But drafting such a proposal is no small task.

To help you on your journey, we’ve got step-by-step instructions and a helpful partnership proposal template .

What’s in this guide :

Why you need a business partnership proposal

How to create a proposal for a business partnership, partnership proposal template & software.

Research shows that 70% of business partnerships fail—and (here’s the good news) a clear agreement is one of the best ways to improve your odds of success.

Oftentimes, partners will equally share the burden of losses and the gift of gains. But your share should reflect what you put into the business, both in terms of time and money. So if one partner will be giving more, they should also get more out of it. By accurately calculating equity, salaries, and profit draws in advance, you can be sure that each partner is getting their fair share according to their initial investment and ongoing role in the company.

A partnership proposal with clear terms can help settle any financial or legal matters that may arise later. But on a more positive note, it will also improve the quality of your collaboration. When all the terms are laid on the table up front (and no one is guessing or assuming), communication between partners will begin with a much stronger foundation—paving the way for a more profitable relationship.

Creating a proposal for your business partnership is complicated, but fortunately, you don’t have to go it alone. Follow these simple steps to cover all of your bases.

Step 1. Research what your proposal should include

The first step is to research what you need to include in your proposal, such as the share of profit and loss, the managing duties of each partner, and what should happen in the event of the death of a partner. This is a critical legal document so you need to get it right..

You don’t have to get it perfect the first time, as the terms will likely require negotiation. But covering all of the necessary information will demonstrate your attention to detail and ensure that the preceding negotiations are thorough.

Make sure to research requirements that are unique to your partnership type , which usually falls into one of these 3 categories:

General partnership - Shared day-to-day operations and liability for debts and owners.

Limited partnership - One or more partner doesn’t participate in day-to-day operations and is not liable for debts or lawsuits (but receives profits). This is typically used for inactive investors.

Limited liability partnership - Liability protection is extended to all partners so that no one is responsible for the actions of another partner. This is typically used for professionals operating out of shared office space, such as accountants, financial advisors, or plastic surgeons.

Because the taxation structure will affect the way that earnings are distributed and reported, you should also research details specific for your province or state of incorporation as well as your entity type (limited liability corporation, c-corp, etc.).

Brainstorm more information to include based on your unique business and what each partner brings to the table. For instance, if one partner is joining the partnership with a large social media following of ideal customers, you might want to outline how that social media account is expected to be used and what content will not be permitted on that account once the partnership begins.

If you use a partnership proposal template, you’ll save a lot of time on both research and writing. Preview our template here.

Make sure to consult with a business lawyer to get their take on the necessary terms.

Step 2. Outline your proposal

Now that you have your checklist for what to include in your proposal, it’s time to start organizing all of that information into a cohesive outline. A proposal template will save you time here. Start off with the template and then include additional terms that matter to your business.

We suggest this outline for your partnership proposal:

Name and Business - Basic business details like business name and address.

Term - When the agreement begins.

Capital - How partnership capital will be maintained.

Profit and Loss - How profits and losses will be shared and credited.

Salaries and Drawings - How salaries and profit draws will be managed.

Interest - Whether or not initial investments will receive guaranteed interest payments.

Management Duties and Restrictions - How management duties will be split, and what tasks can’t be undertaken without agreement from all partners.

Banking - What chequing account(s) will be used.

Books - How bookkeeping will be managed.

Voluntary Termination - How the partnership can be voluntarily dissolved, and how assets will be distributed if this occurs.

Death - What will happen in the event of the death of a partner.

Arbitration - Basic statement on arbitration for the agreement and the legal association that will be used.

You might be wondering if you need to add a cover letter to your outline. If you don’t need to convince anyone to join the founding team, you probably don’t need a cover letter. But if you’re trying to win over a partner, then check out this guide to writing a cover letter and add your letter to the very beginning of your proposal.

Step 3. Write the proposal sections

Time to write.

A partnership proposal has a very different style than most other business proposals , which are typically sent to prospective clients in order to win deals. For those proposals, you’re trying to sell . But with a partnership proposal, you’re trying to clarify . The prospective partner needs to know what they’re signing off on in order to give you a yes. What’s expected of them? What percentage of equity will they receive?

Because the goal is different, the writing style should be different too. Write using clear, simple, and legally accurate language for the majority of the proposal. By keeping the language of the proposal straightforward , you’ll eliminate any confusion and potential for disagreements later.

Take this text from our partnership agreement template as an example of the writing style you should aim for:

A separate capital account shall be maintained for each partner. Neither partner shall withdraw any part of his/her capital account. Upon the demand of either partner, the capital accounts of the partners shall be maintained at all times in the proportions in which the partners share in the profits and losses of the partnership.

If you need to create content to convince on-the-fence partners, you can do so with your cover letter, business plan, or presentation slides that will go along with the proposal. You might cover the addressable market, your competitive advantage, pricing model, etc.

Step 4. Add e-signatures

The next step is to add e-signatures to your proposal. This will turn the proposal into a binding agreement, so that once signed by all partners, the partnership can begin with clear terms.

You should add the e-signatures to the final page of the proposal.

Make sure that the e-signature software you use is legally binding .

Step 5. Review, sign, and send it

And lastly, it’s time to make sure your proposal is perfect. Review all of the terms and make sure you’ve covered everything in your checklist.

If you can afford it, have a business lawyer review your agreement before you sign and send it. This should be cheaper than having them draft an agreement from scratch (and can save you a lot of money and stress in the long run).

When you’re ready, sign the proposal yourself and then send it for signature to your partners.

You should not open up any bank accounts, file articles of incorporation, take out loans, or conduct any other activity with financial implications until the proposal is signed by all partners. If you do, a partner could later argue that they’re not liable. Instead, use the time before the proposal is signed to work on your business plan and research your addressable market.

Proposify makes it easy to create beautiful proposals for both internal and external use. We offer 75 unique proposal templates that show you exactly what to include and help you draft your proposals quickly.

You can also design your own proposal templates, save content snippets, and track stats on proposal views and closed deals.

Dayana Mayfield is a B2B SaaS copywriter who believes in the power of content marketing and a good smoothie. She lives in Northern California. Connect with her on LinkedIn here: linkedin.com/in/dayanamayfield/

Subscribe via Email

Related posts.

| All accounts allow unlimited templates. | |||

| Create and share templates, sections, and images that can be pulled into documents. | |||

| Images can be uploaded directly, videos can be embedded from external sources like YouTube, Vidyard, and Wistia | |||

| You can map your domain so prospects visit something like proposals.yourdomain.com and don't see "proposify" in the URL | |||

| Basic | Team | Business | |

| All plans allow you to get documents legally e-signed | |||

| Allow prospects to alter the quantity or optional add-ons | |||

| Capture information from prospects by adding form inputs to your documents. | |||

| Basic | Team | Business | |

| Get notified by email and see when prospects are viewing your document. | |||

| Generate a PDF from any document that matches the digital version. | |||

| Get a full exportable table of all your documents with filtering. | |||

| Basic | Team | Business | |

| Connect your Stripe account and get paid in full or partially when your proposal gets signed. | |||

| Create your own fields you can use internally that get replaced in custom variables within a document. | |||

| All integrations except for Salesforce. | |||

| You can automatically remind prospects who haven't yet opened your document in daily intervals. | |||

| Lock down what users can and can't do by role. Pages and individual page elements can be locked. | |||

| Create conditions that if met will trigger an approval from a manager (by deal size and discount size). | |||

| Use our managed package and optionally SSO so reps work right within Salesforce | |||

| Our SSO works with identity providers like Salesforce, Okta, and Azure | |||

| Great for multi-unit businesses like franchises. Enables businesses to have completely separate instances that admins can manage. | |||

| Basic | Team | Business | |

| Our team is here to provide their fabulous support Monday - Thursday 8 AM - 8 PM EST and on Fridays 8 AM - 4 PM EST. | |||

| Sometimes the written word isn't enough and our team will hop on a call to show you how to accomplish something in Proposify. | |||

| Your own dedicated CSM who will onboard you and meet with you periodically to ensure you're getting maximum value from Proposify. | |||

| We'll design your custom template that is built with Proposify best-practices and train your team on your desired workflow. | |||

| Our team of experts can perform advanced troubleshooting and even set up zaps and automations to get the job done. |

Subscribe via email

- Crafting an Effective Partner Business Plan: Essential Elements for Success

Share this article

Print/Download PDF

By Harrison Barnes

Rate this article

922 Reviews Average: 5 out of 5

Discuss Partners on Top Law Schools

- ideas on how to network with judge's son who is partner?

- Networking/taking a partner at a firm out to lunch?

- NYC Study Partners- for those truly motivated

- 165+/Retake Study Partner?

- Arizona Study Partner

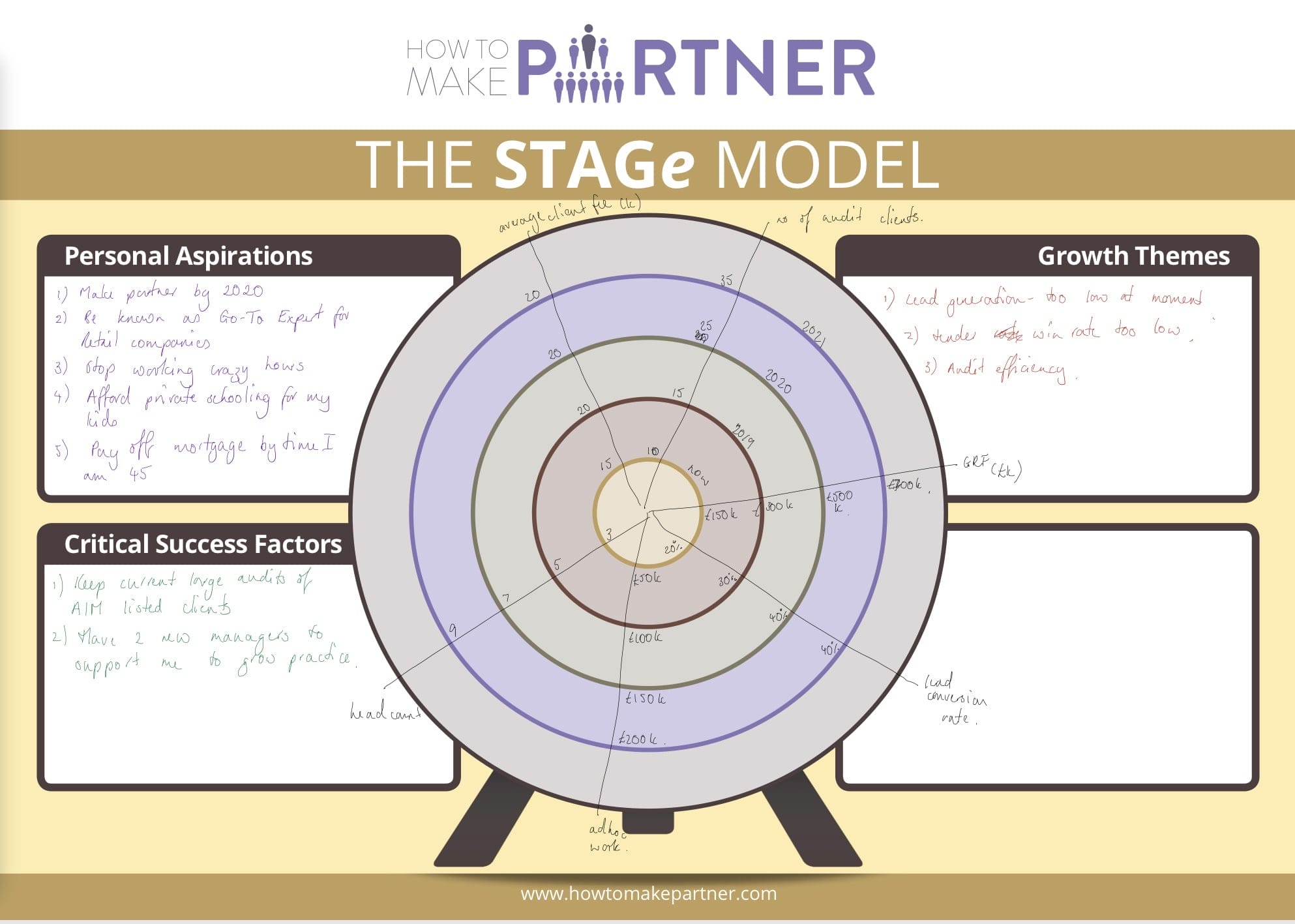

Partner Business Plans: Key Elements

- The Crucial Role of Business Plans in Law Firm Partner Success

- Maximize Portables in Your Business Plan in Order to Maximize Interest in You

The Importance of a Great Business Plan

Professional Goals For Partner Status

Making an evaluation of your existing practice, describing your vision as a partner, creating a strategy for growth.

- A partner's fit culturally

- The viability of a partner's practice for the long-term

- A partner's record of excellent client service to long-term clients and producing business

- A partner's history of consistently increasing collections

- A partner's practice fit in connection with the firm's strategic plan for expansion

- Whether a partner's practice area is one that is targeted for growth

- Whether the partner brings portable business and/or specific expertise needed in a particular practice area

- The opportunities the partner would bring for business development and significant cross-selling were the partner to join the firm

- Whether the partner's historical information is reflective of consistent productivity

- Whether the partner's client base fits within the firm's client structure

- Any potential conflicts that would preclude the firm from hiring the partner

- A partner's current compensation and compensation expectation

- A partner's potential contribution to the firm's bottom line/profitability

- A partner's fit within the firm's current attorney roster

- A partner's reason for leaving his or her current firm (voluntary/mutual arrangement) and whether the partner would be a problem

- Creative: Serve as a marketing piece on the partner and enable the firm to assess the partner's business potential. It should also provide an outlet to the partner to step out of the resume format and chart his or her previous performance and future prospects for business in a creative format.

- Illustrative: Illustrate to a firm that the partner is thinking about his or her practice as a business and set forth his or her plan for the future.

- Persuasive: Persuade the firm to hire the partner.

- Historical: Chart a historical record of the partner's history of creating business opportunities and his or her ability to develop and foster client relationships over an extended period of time.

- Demonstrative: Demonstrate a partner's business-development skills, initiative, and ability to contribute not only to his or her own success but also to the success of his or her colleagues through cross-selling efforts. It should also demonstrate ways a partner can contribute to a firm's financial bottom line, enhance its practice-group development, and ultimately bring added value to the team.

- Prophetic: Prophesy what the partner believes he or she will be able to accomplish in his or her practice and for the firm in the short and long term.

- Preparatory: Prepare the partner for the interviewing process.

Introduction

- Provide a narrative including professional history, practice overview, and a description of areas of expertise. This section may highlight briefly particular areas of expertise that the firm does not currently have.

- Describe the partner's role historically as a business developer.

- Briefly touch upon why the partner believes he or she would be a good fit for a particular firm.

Market Research/Analysis

- Give analysis of local need for services in partner's practice area.

- Describe local competition/other law firms with similar practices.

- Give overview of need in local market for partners with his or her expertise.

- Describe why partner believes firm provides the best platform in the marketplace for his or her particular practice area.

Current Client Base

- Describe current portable clients (use generic or specific).

- Describe key industries serviced.

- Discuss other partners' clients partner is servicing.

Additional Contacts to Develop

- Discuss contacts not yet tapped.

- Given market analysis, project possible targets in local, regional, national, or international markets.

- Discuss possible expansion of business from current client base.

Cross-Selling Opportunities

- Describe cross-selling opportunities with current clients.

- Describe cross-selling opportunities with known key clients of prospective firm.

- Discuss other practice areas at current firm to which partner is delegating work.

- Discuss services your clients are requesting that you cannot currently service at your firm and could otherwise capture at the new firm .

Other Business-Development Sources

- Describe additional business contacts you are pursuing or plan to pursue

- Speeches, publications

- Community organizations

- Bar associations

- Internal marketing initiatives

- Client seminars/newsletters

Long-Term Strategy Goals and Targets

- Set targets for expansion of practice in terms of collections, attorneys, and clients/industries.

- Consider possibility of local to regional to national growth patterns.

- Consider growth in other key competencies which may be affected by partner's long-term success.

- Discuss long-term strategies in connection with firm's overall strategic plan and practice-group development plans.

Historical Collections, Billing Rates, and Billable Hours

- If a partner with a lower billing rate structure, chart the anticipated rate increases by portable client or anticipated timeline for rate increases to current clients. Discuss any alternative billing arrangements you currently have in place with clients.

- Include three-year client collections history by client (as originating attorney and as billing attorney on other attorneys' matters). Include projection for current fiscal year.

- Include three-year billing rate history.

- Include three-year historical compensation history (including bonus information).

- Include three-year billable hour history.

- Note pending projects contributing to future collections.

- Include a summary of anticipated collection projections for the next three to five years.

- Business-development budget

- Time commitments from partners in other practice areas for cross-selling purposes

- Key staff needed (secretary, paralegals, etc.)

- Foreign-language skill requirements

- Travel expenses

- Marketing materials, presentations, etc.

Creative Conclusion

- Recap key points in plan, added value partner brings, and reasons he or she would be a good fit.

- Emphasize flexibility of plan and eagerness and willingness to discuss and modify in accordance with firm's plans and objectives.

- See 30 Ways to Generate Business as an Attorney for more information.

Want to continue reading?

Become a free bcg attorney search subscriber..

Once you become a subscriber you will have unlimited access to all of BCG’s articles.

There is absolutely no cost!

Harrison Barnes does a weekly free webinar with live Q&A for attorneys and law students each Wednesday at 10:00 am PST. You can attend anonymously and ask questions about your career, this article, or any other legal career-related topics. You can sign up for the weekly webinar here: Register on Zoom

Harrison also does a weekly free webinar with live Q&A for law firms, companies, and others who hire attorneys each Wednesday at 10:00 am PST. You can sign up for the weekly webinar here: Register on Zoom

You can browse a list of past webinars here: Webinar Replays

You can also listen to Harrison Barnes Podcasts here: Attorney Career Advice Podcasts

You can also read Harrison Barnes' articles and books here: Harrison's Perspectives

Harrison Barnes is the legal profession's mentor and may be the only person in your legal career who will tell you why you are not reaching your full potential and what you really need to do to grow as an attorney--regardless of how much it hurts. If you prefer truth to stagnation, growth to comfort, and actionable ideas instead of fluffy concepts, you and Harrison will get along just fine. If, however, you want to stay where you are, talk about your past successes, and feel comfortable, Harrison is not for you.

Truly great mentors are like parents, doctors, therapists, spiritual figures, and others because in order to help you they need to expose you to pain and expose your weaknesses. But suppose you act on the advice and pain created by a mentor. In that case, you will become better: a better attorney, better employees, a better boss, know where you are going, and appreciate where you have been--you will hopefully also become a happier and better person. As you learn from Harrison, he hopes he will become your mentor.

To read more career and life advice articles visit Harrison's personal blog.

Article Categories

- Legal Recruiter ➝

- Attorney Career Advice ➝

- Advice for Partners ➝

- Business Plans

Do you want a better legal career?

Hi, I'm Harrison Barnes. I'm serious about improving Lawyers' legal careers. My only question is, will it be yours?

About Harrison Barnes

Harrison is the founder of BCG Attorney Search and several companies in the legal employment space that collectively gets thousands of attorneys jobs each year. Harrison is widely considered the most successful recruiter in the United States and personally places multiple attorneys most weeks. His articles on legal search and placement are read by attorneys, law students and others millions of times per year.

Find Similar Articles:

- strategic Partnerships

- risk Analysis

- regulatory Compliance

- professional Development

- Partner Business Plans

- legal Advice

- law Firm Planning

- governance Strategies

- goal Setting

- financial Management

- crisis Management

- corporate Structure

- contract Negotiation

- conflict Resolution

- business Law

Active Interview Jobs

Featured jobs.

Location: New York - Inwood

Location: Pennsylvania - Yorklyn

Location: California - Encino

Most Viewed Jobs

Location: Massachusetts - Boston

Location: Texas - Austin

Location: New York - New York City

Upload Your Resume

Upload your resume to receive matching jobs at top law firms in your inbox.

Additional Resources

- Harrison's Perspectives

- Specific Practice Areas

- The Winning Mindset

BCG Reviews

Thanks! You guys helped me find a job so that's the best benefit! I loved working with Patrick he was very nice, profess.... Read more >

Mara Peterson

University of North Carolina School of Law

One of my favorite things about working with BCG was the ease of the processes, even doing it long distance.I was given .... Read more >

Elizabeth Hall

Emory University School of Law, Class Of 2011

I thought that the two [recruiters] I worked with were both very helpful and knowledgeable, both in terms of our phone c.... Read more >

James Geiser

University of Michigan Law School, Class Of 2016

My favorite thing about working with BCG was my legal placement professional. She was very invested in my search and got.... Read more >

Mauricio Gonzalez

Cornell, Class Of 2003

My legal placement professional was friendly and responsive and seemed to really know the market and understood what I w.... Read more >

Robyn Lesser

Barry University Dwayne O. Andreas School of Law, Class Of 2011

I really liked the recruiter I worked with and her experience and I appreciated her ability to guide me through the proc.... Read more >

Jonathan Nye

Suffolk University Law School, Class Of 2008

Popular Articles by Harrison Barnes

- What is Bar Reciprocity and Which States Allow You to Waive Into the Bar?

- What Do Law Firm Titles Mean: Of Counsel, Non-Equity Partner, Equity Partner Explained

- Top 6 Things Attorneys and Law Students Need to Remove from Their Resumes ASAP

- Why Going In-house Is Often the Worst Decision a Good Attorney Can Ever Make

- Top 9 Ways For Any Attorney To Generate a Huge Book of Business

Helpful Links

- The BCG Attorney Search Guide to Basic Law Firm Economics and the Billable Hour: What Every Attorney Needs to Understand to Get Ahead

- Quick Reference Guide to Practice Areas

- Refer BCG Attorney Search to a Friend

- BCG Attorney Search Core Values

- Recent BCG Attorney Search Placements

- What Makes a World Class Legal Recruiter

- What Makes BCG Attorney Search The Greatest Recruiting Firm in the World

- Top 10 Characteristics of Superstar Associates Who Make Partner

- Off-the-Record Interview Tips From Law Firm Interviewers

- Relocating Overseas

- Writing Samples: Top-12 Frequently Asked Questions

- The 'Dark Side' of Going In-house

- "Waive" Goodbye To Taking Another Bar Exam: Typical Requirements and Tips to Effectively Manage the Waive-in Process

- Changing Your Practice Area

- Moving Your Career to Another City

- A Comprehensive Guide to Working with a Legal Recruiter

- A Comprehensive Guide to Bar Reciprocity: What States Have Reciprocity for Lawyers and Allow You to Waive into The Bar

Related Articles

A Career Guide for Law Firm Partners

Practice Management

Marketing Your Law Firm Through Practice Groups

Related Video

- What is a Counsel and How does it Compare to a Partner�

Related Podcast

- How Any Attorney Can Get a $100+ Million Book of Business, Become a Partner in a Major Law Firm, or Start a Successful Business and Retire Whenever They Want�

When you use BCG Attorney Search you will get an unfair advantage because you will use the best legal placement company in the world for finding permanent law firm positions.

Don't miss out!

Submit Your Resume for Review

Register for Unlimited Access to BCG

Sign-up to receive the latest articles and alerts

Already a subscriber? Sign in here.

- Design for Business

- Most Recent

- Presentations

- Infographics

- Data Visualizations

- Forms and Surveys

- Video & Animation

- Case Studies

- Digital Marketing

- Design Inspiration

- Visual Thinking

- Product Updates

- Visme Webinars

- Artificial Intelligence

12 Best Business Partnership Proposal Templates to Streamline Collaboration

Written by: Idorenyin Uko

Strategic partnerships are critical to any growth-focused business strategy.

But one thing’s for sure: landing the right strategic partnership isn't a walk in the park.

Without the right proposal template, you may struggle to create a well-written and hyper-targeted business partnership proposal that communicates the benefits of the proposed collaboration.

That’s why we’ve rounded up 12 business partnership proposal templates to streamline your collaboration. Our proposal templates will save you time and effort by providing a predefined structure, content, visuals and design. With a few clicks, you can easily create a professional-looking partnership proposal in minutes.

We will also discuss how to write a winning business partnership proposal.

Ready? Let’s get to it!

Table of Contents

What is a business partnership proposal, 12 business partnership proposal templates, how to write a proposal for business partnership, partnership proposal faqs.

- A partnership proposal is a written document that outlines a business' desire to form a partnership or joint venture with another company.

- Visme offers extensive templates to help you create impressive partnership proposals in minutes.

- To write a proposal for a business partnership, research your prospective partner, choose a customizable proposal template , write the content, customize your proposal, add interactive elements and download and share it with your prospective partners.

- Use Visme’s proposal maker to create killer partnership proposals that attract partners and drive business growth.

A business partnership proposal is a document that outlines the details of a potential collaboration between two or more businesses.

This type of business proposal is written by a company that wants to enter into a partnership, collaboration or joint venture with another company.

The aim of writing a partnership proposal is to demonstrate interest in doing business with the proposed partner and to convince them that the collaboration would benefit all parties.

Business partnership proposals typically detail the objectives, goals and benefits of the partnership, as well as the roles and responsibilities of each partner. The proposal also specifies the terms of the agreement and any financial obligations that may arise from the partnership.

Having a partnership proposal aligns the interests of both the proposing entity and potential partners, ensuring they are on the same page and know what’s expected of them. It provides a written record of the agreed-upon terms and conditions, which can be revisited to ensure that both parties stay aligned with their agreements.

RELATED: 12 Best Business Partnership Proposal Templates to Streamline Collaboration

In this section, we’ve rounded up 12 customizable business partnership templates to get you started. These templates are professionally designed and span a wide range of industries.

Here’s what one of our users had to say about Visme templates.

1. Retail Store Partnership Proposal

Put your best foot forward when proposing a partnership with this beautiful business proposal template. This partnership proposal features the company, value proposition, partnership details, what each partner gets, next steps and terms and conditions.

With an energetic orange color theme and stunning images, this template is sure to create a strong impression on your potential partners.

The beautiful images are strategically placed across all the pages to break up text and add visual appeal, while the geometric shapes add a dynamic and modern touch. You can easily customize this template to suit your unique needs. Swap the content with your own, change colors, fonts and images and even input your own logo.

2. Partnership Proposal Letter

Demonstrate a serious and committed approach to the proposed partnership with this proposal letter. Not only does this business partnership proposal letter lay the foundation for a successful collaboration, but it also facilitates discussions, negotiations and ongoing communication.

The opening paragraph introduces the company, while the body of the letter dives into the proposal for collaboration and its benefits. Towards the end of the letter, there's ample space for you to sign off or provide your contact details so prospects can easily reach out.

Overall, the document maintains a clean and organized appearance and is divided into well-structured paragraphs, each addressing different aspects of the partnership proposals. The color scheme is professional, combining corporate grays and subtle accents of muted green.

Add a touch of elegance by designing a clean header with your company's name and logo. With Visme’s free letterhead maker , you can design branded letterheads in minutes. And if you don’t have a logo, Visme has a free logo maker you can use to quickly make one.

3. Organizational Partnership Proposal

Looking to get potential partners enthusiastic about collaborating with your organization? This partnership proposal has everything you need.

It’s designed with the healthcare industry in mind, but you can easily customize it for other industries as well—pharmaceuticals, nonprofits, manufacturing and more. The template features an executive summary along with the partnership's objectives, benefits, impact and process.

These key sections clarify the terms and expectations of the partnership, minimizing misunderstandings and ensuring that both parties are on the same page.

When it comes to visuals, this business partnership proposal template is a masterpiece. Each section of the proposal is clearly defined with orange-colored blocks or borders. The rich blend of white and shades of green gives the templates an elegant feel.

These designs not only guide the reader but also add a cohesive look to the overall document. Spice up your partnership proposals with beautiful icons , photos and videos —all sourced from the Visme library.

4. Partnership Investment Proposal

This eye-catching partnership investment proposal template is your golden ticket to attracting big investors to fund or partner with your business. The collaborative goals provide a clear direction for the partnership. Also, the proposed partnership framework, investment opportunity, SWOT analysis and exit strategies are clearly communicated.

With these key sections, all parties have a mutual understanding regarding their roles, responsibilities and expectations. It can also serve as a key performance indicator to measure progress, assess performance and make data-driven decisions.

This proposal offers a visual experience that leaves a positive and memorable impact. The cover page sets the tone with a seamless blend of deep purple transitioning into a radiant yellow gradient. On the rest of the pages, the sprinkle of icons, characters and images enhances its overall visual appeal.

If you don’t find the perfect visuals, tap into Visme’s AI image generator . Just describe what you want to create and watch the tool generate your unique visuals in seconds. You can choose from several output styles—photos, paintings, pencil drawings, 3D graphics, icons, abstract art and more.

5. Finance Consultancy Partnership Proposal

Show potential business partners why they should grab the opportunity to collaborate with your company. It includes information about your company, achievements, what the proposed partnership is about and what they’ll get, as well as your responsibilities, next steps and FAQs.

The trendy design layout makes this sample business partnership proposal stand out. It features monochrome images, exciting colors, high-res stock images, colorful icons and professional fonts—everything you need in a well-rounded partnership proposal template.

If you have custom images you want to use in your proposal that need editing, Visme’s AI Edit Tools can help. You can edit, touch up, unblur and upscale your photos with a single click; no design or coding needed.

6. Management Company Partnership Proposal

Looking to drive business growth through strategic business partnerships? This creative business partnership proposal template has everything you need to seal your next big partnership deal.

The captivating color palette and thoughtfully designed layout ensure that you leave a lasting impression on potential partners. This template's stunning visual appeal doesn't just stop there; it seamlessly directs attention to your textual content.

It features several customizable pages covering critical sections of your proposed partnership models, terms and conditions and company history—everything required to showcase your brand services and why the client should choose your company over others.

Another upside of using Visme is that you can easily customize any copy to your brand and purpose. Visme’s AI writer lets you craft engaging copy for your partnership proposal in seconds. Provide a detailed prompt with more context and watch the tool unleash its magic.

7. Music School Partnership Proposal

Create a partnership proposal that stands out from the rest with this music-themed proposal template. With dedicated pages for breaking down musical services, sharing testimonials and outlining expenses, this template makes it easy for clients to understand the scope of your services and how you can help them achieve their musical goals.

This template combines sleek design elements, high-quality vector icons and stunning stock photos to showcase your music agency's unique style and professionalism.

Notice how the business partnership proposal template deploys stunning images of musical instruments. Each photograph is carefully chosen to complement the purple color scheme, creating a visually cohesive and aesthetically pleasing experience.

If you’re short on time and need your proposal ready in seconds, you can use Visme’s AI Document Generator . Just describe the document you want to create in detail and the chatbot will recommend styles. Choose the one you like that matches your topic and brand and let AI create your design.

Visme lets you fully customize your project. You can select a color theme, adjust text, add photos, videos and graphics from Visme’s free assets library or generate new ones with Visme AI tools.

8. Fashion Brand Partnership Proposal

Set the tone for a mutually beneficial relationship using this dazzling partnership proposal template.

This fashion-themed template boasts a stunning color scheme complemented by a sophisticated font selection that will undoubtedly draw attention to your content. The fashion sketches and illustrations of models wearing lilac-inspired outfits embody the essence of your fashion brand.

Use it to communicate what your brand is about, its services, the benefits of partnering with your brand and the terms and conditions with prospective partners. To make this template your own, simply replace the placeholder text with yours and select from a variety of visual assets to enhance it.

Keep your proposal and other projects on brand with the help of Visme’s brand wizard . Just input your website and the tool will grab your brand assets and save them to your brand kit. That way, you don’t have to manually set your branding whenever you work on a design project.

9. Partnership Proposal

Craft a compelling business partnership proposal that showcases the benefits of collaborating with your company using this visually appealing template. With ample whitespace and a clean design, this template allows you to focus on the substance of your proposal and effectively communicate your vision for a successful partnership.

It has a captivating design with a bold color scheme, striking vector icons and high-resolution stock images that you can easily replace to suit your needs. Turn your document into an immersive experience with animation and interactive elements .

With pop-ups and hover effects, you can easily provide more information without overwhelming your audience. Moreover, you can link content blocks or pages of your proposal to a particular page on your website.

10. Finance Consulting Partnership Proposal Presentation

If you’re looking to present your proposal to stakeholders, this presentation template is what you need. This template is a premier choice for financial professionals, including consultants, CFOs and businesses seeking to cultivate meaningful partnerships.

With its user-friendly interface and eye-catching visuals, your proposal is certain to make a lasting impression on potential partners. It features dedicated sections for company profiles, service offerings, case studies, notable achievements and partnership proposals.

The template's contemporary aesthetic—complete with fresh fonts, vibrant colors and insightful charts, graphs and infographics—streamlines the process of presenting complex financial analysis and revenue projections.

If you need your presentation ready in minutes, Visme's AI presentation maker can come in handy. It lets you create ready-to-use presentations in a fraction of the time. Not only does the tool cut down on content production time, but it also makes the entire process convenient.

11. Payment App Brand Collaboration Proposal

If you’re looking for a tech or fintech-related proposal that will attract potential partners for your business, look no further! Our brand collaboration proposal template is designed to help you showcase the advantages of your payment app and present a persuasive partnership proposal to potential collaborators.

With high-quality graphics, smart design elements and engaging font styles, this template will make a lasting impression. The template includes vital sections such as project objectives, payment app features, statistics and proposed partnership alignment, enabling you to present your proposal meticulously.

Confidently demonstrate the value your payment app can bring to potential partners and secure the collaborations you need to take your business to the next level.

If you’re working on the proposal with your team, Visme streamlines collaboration across teams of all sizes. You can add team members to your project, control permissions and enable real-time editing.

The workflow management feature helps you manage projects easily in Visme. Team members can edit, leave feedback, reply and resolve comments in real-time. Assign projects to team members, set deadlines, manage roles and track progress all in one place.

12. Sports Brand Collaboration Proposal

Looking to make a splash in the sports industry? Our athletic-themed collaboration proposal template is an excellent pick. This powerful template is designed to help you stand out among competitors and engage potential sports partners.

From brand history to partnership objectives, benefits and a clear collaboration structure, this template contains key information for a winning partnership proposal. The stunning visuals, dynamic design elements and tailored content for the sports industry will help solidify your brand's presence and make a lasting impression on your potential partners.